Last year the number was 152,355. We said so, on this exact page. Then iblead.com lifted it word for word in December. Funny thing about a number you pull from live Google Maps data, though — it doesn't sit still. Today Scrap.io counts 161,021 money transfer services in the United States. That nine-thousand jump in a few months? That's the whole argument against buying a static money transfer service email list in one statistic.

Video: Get Emails from Google Maps for Free — Scrap.io Tutorial

📋 What's in this guide

- The Money Transfer Industry: 2026 Market Overview

- 161,021 US Money Transfer Services: Fresh Data from Scrap.io

- Major Money Transfer Companies

- Why Traditional Email Lists Fail in the Money Transfer Sector

- Building Compliance-First Email Lists for Financial Services

- Geographic Distribution: Where Money Transfer Services Thrive

- B2B Use Cases: Who Targets Money Transfer Services?

- Fresh Data Extraction vs Purchased Email Lists

- Legal Compliance: GDPR, CCPA, and Financial Regulations

- Getting Started: Your Money Transfer Email List Strategy

- Frequently Asked Questions

Here's a story I think about a lot. A fintech founder I know spent three months trying to build partnerships with money transfer operators. He bought what looked like a "premium" financial services database for $1,200. Ten thousand contacts. Looked the part. Half bounced before he'd finished his coffee, another quarter went to people who'd left their firms months earlier, and the survivors were compliance officers who do not, as a rule, enjoy mystery email from vendors they've never heard of. Two real conversations. That was the haul.

So that's where we start. Not with the size of the market — with the bounce report. Because the money transfer sector is genuinely booming, and most people trying to reach these businesses are still using data that rotted on a shelf.

Let's fix that.

The Money Transfer Industry: 2026 Market Overview

Some numbers, then. The global money transfer services market sits at roughly $49.29 billion in 2026 and is forecast to reach $123.23 billion by 2033 — a 16.5% compound annual growth rate, according to Coherent Market Insights. North America holds about 27.5% of that market in 2026. So when people say this sector is "growing," they're underselling it.

Now zoom in on the digital side, because that's where the budgets are moving. Digital remittance is projected to grow at a brutal ~27.6% CAGR — from $16.79 billion in 2026 to $150.53 billion by 2035 (Business Research Insights). Mobile-first transfers, real-time rails, blockchain settlement. Everyone's rebuilding their stack at once.

And the macro picture underneath all of this? Remittances. Officially recorded flows to low- and middle-income countries hit roughly $685 billion in 2024, with about $690 billion projected for 2025 (World Bank / KNOMAD). That's bigger than foreign direct investment and official aid combined. In fact remittances have been the single largest source of external finance for these countries (excluding China) since 2015. Read that twice.

The corridors tell you where the money actually goes. In 2024 the top recipients were India ($129 billion), Mexico ($68 billion), China ($48 billion), the Philippines ($40 billion), and Pakistan ($33 billion) — again, World Bank, 2024. Behind every one of those flows sits a chain of businesses processing, facilitating, and supporting the transfer. They all buy software. They all buy compliance. They all need somebody.

That somebody might be you. Question is whether you can reach them.

161,021 US Money Transfer Services: Fresh Data from Scrap.io

Ask a traditional list vendor how many money transfer services operate in the US and watch them stall. Most genuinely don't know — they sell whatever was in last quarter's export. We do know. Pulled live from Google Maps right now: 161,021 money transfer service establishments across the United States.

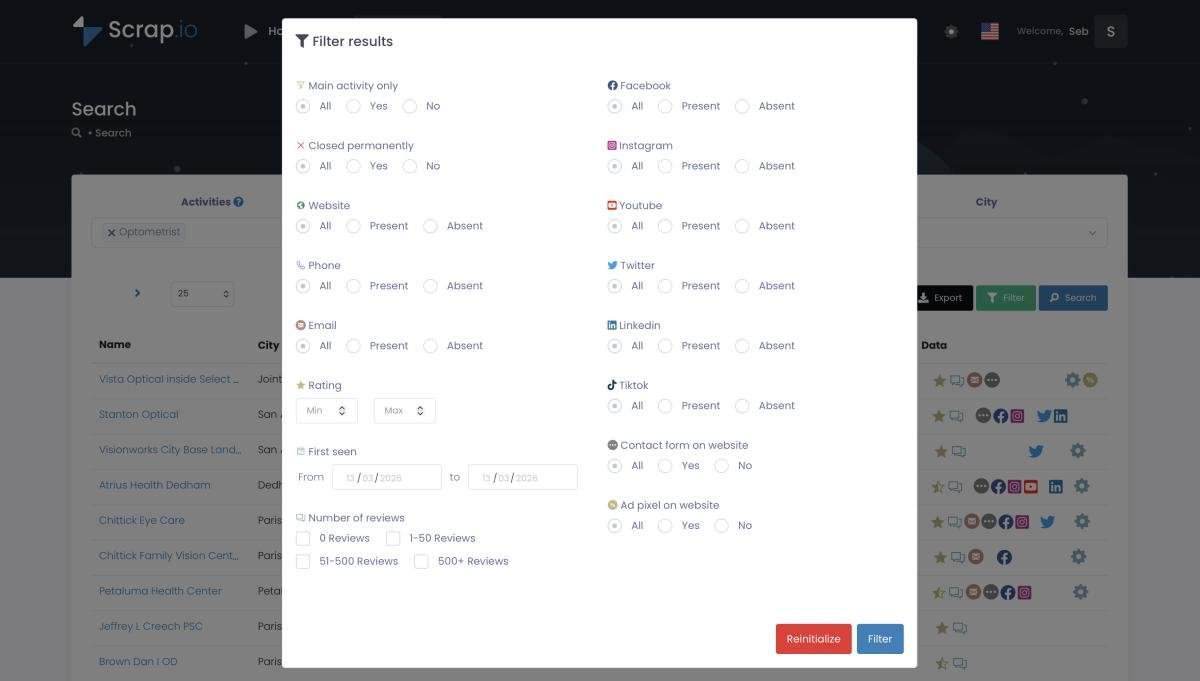

And here's the part that actually matters for your budget: 106,658 of them have an email address on file. You can filter for exactly those before you spend a single credit, which means you're never paying to "discover" that a listing has no contact info. (More on why that filter is the whole ballgame in a minute.)

The rest break down in ways worth understanding. A big share are dedicated operators — Western Union agents, MoneyGram locations, independent money transmitters living and breathing remittances. Those are your hot prospects, the kind you'd want on a money transmitter email list or an MSB email database. Then there's the long tail: convenience stores, check-cashing spots, and corner shops that offer transfers as a side hustle. Different decision-makers. Different budgets. Same Google Maps listing format, totally different pitch.

Video: How to Scrape Google Maps at the Country Level — Scrap.io

The beauty of pulling this from Google Maps? It's alive. New operator opens, updates their hours, swaps a phone number — captured. You're not emailing a business that shut its doors in March. That's how 152,355 became 161,021 in the span of a couple of quarters, and it's why "how many money transfer services in the us" is a question only live data can answer honestly.

Curious how many sit in your state? The count is free — Scrap.io never charges credits to count results, in the app, the API, or the MCP. See the number for your target market before you commit a cent.

Major Money Transfer Companies: From Western Union to Remitly

Know the big players and you'll know who to sell to — and how. The market is in open recomposition, which is exactly where B2B opportunity hides.

Remitly took the lead with roughly 23% market share as of late 2024. Not bad for a company that launched in 2013. Western Union is still the name your grandmother trusts, present in 200+ countries — and scrambling to modernize legacy systems that creak under every new compliance rule. MoneyGram runs hundreds of thousands of agent locations worldwide. PayPal's Xoom rides the PayPal base. Wise keeps eating the cross-border SMB segment. Ria sits comfortably among the global top three. (Market share figures shift constantly; treat these as a late-2024 snapshot, not gospel. For a fuller cast list, finder.com keeps an A-to-Z of providers.)

What does the churn mean for you? Everything. Incumbents need to modernize. Newcomers need infrastructure. Both need compliance, marketing, and operational tooling — yesterday.

A market that's settled is a market that's closed. This one's wide open.

Why Traditional Email Lists Fail in the Money Transfer Sector

Let's be blunt: most purchased financial-services lists are garbage in this niche. I've watched it fail too many times to be polite about it.

The data's ancient. Money transfer agents switch networks, independents pivot providers, storefronts open and close on the immigration economy's rhythm. A list that was accurate six months ago is fiction now. Most email list providers refresh quarterly at best.

The targeting is also too blunt. A generic "financial services" b2b email list — or any off-the-shelf business email database — dumps money transmitters in the same bucket as banks, insurers, and RIAs, like shelving sushi next to motor oil because both come in containers. Try getting a clean list of money transfer companies in the USA, or a real remittance companies contact database, out of one of those. You can't. And the quality? One compliance vendor I know bought a "verified" financial list of 10,000. Maybe 3,000 were actually at money transfer services. The rest had zero buying authority.

This is the community consensus, not just my grumbling. Scan r/Emailmarketing or r/sales for five minutes and you'll see the same verdict, paraphrased a hundred ways: buying pre-made B2B lists is usually money set on fire. As one recurring complaint puts it — "Bought a 'verified' financial services list. Out of 10k, maybe 3k were relevant, and the rest had zero buying authority." Sound familiar?

Here's the same agency horror story I keep coming back to. A marketing shop that specializes in money transfer clients bought three "premium" lists over eight months. Combined cost: north of $3,000. Combined yield: two qualified conversations. Two. Then they switched to fresh extraction and the difference wasn't subtle.

| Criterion | Purchased Email List | Fresh Google Maps Data |

|---|---|---|

| Data age | 3–12 months old | Updated in real time |

| Category accuracy | Vague "financial services" | Precise — money transfer only |

| Business status | Unverified (open? closed?) | Live verification at export |

| Exclusivity | Resold to your competitors | Pulled fresh, just for you |

| Compliance trail | Murky source | Traceable to public listing |

If you're weighing whether to buy email lists in 2026 at all, that table is most of the answer. Stale beats nothing, barely. Fresh beats stale by a mile.

Building Compliance-First Email Lists for Financial Services

Now it gets serious. You can't blast money transfer operators the way you'd spray a SaaS startup list. This sector is regulated to the teeth, and compliance isn't a checkbox here. It's survival.

Start with the source. Using publicly available information — the contact details a business chose to publish on Google Maps and its own website — puts you on solid ground. They published it. That creates implied permission for legitimate business contact. GDPR matters the moment you touch any EU-connected operator, and plenty handle international corridors. CCPA matters because California is a remittance powerhouse for Latin American transfers. CAN-SPAM applies to every commercial email you send, full stop.

Then layer on the part most people miss: money transmitters carry extra regulatory weight. They're licensed in most states, they report to FinCEN, they live under Bank Secrecy Act obligations. These are people who can smell a sketchy email from space — and who have actual regulators on speed dial.

So the smart approach writes itself. Use only public data. Identify yourself clearly — real name, real address, real reply-to. Make opt-out genuinely easy, not buried. Keep records of where every contact came from. If you want the full playbook, our guide on anti-spam best practices walks through it. The nice byproduct of extracting from Google Maps is that you start compliant by default — you're using data businesses voluntarily made public.

Geographic Distribution: Where Money Transfer Services Thrive

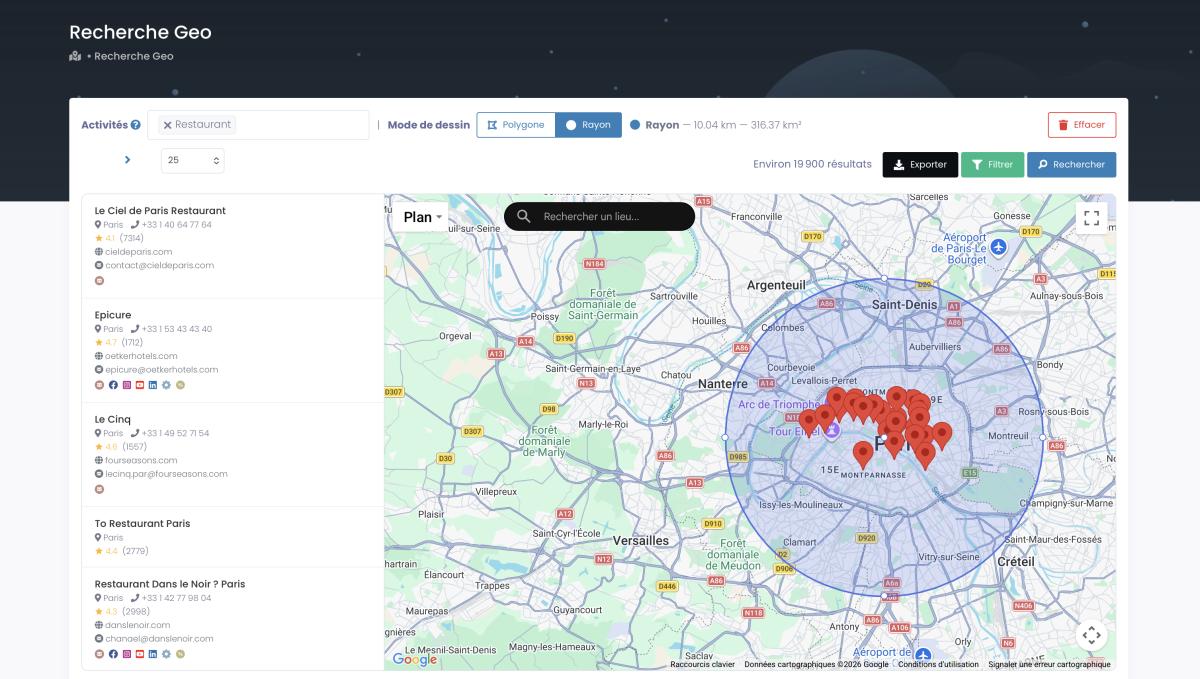

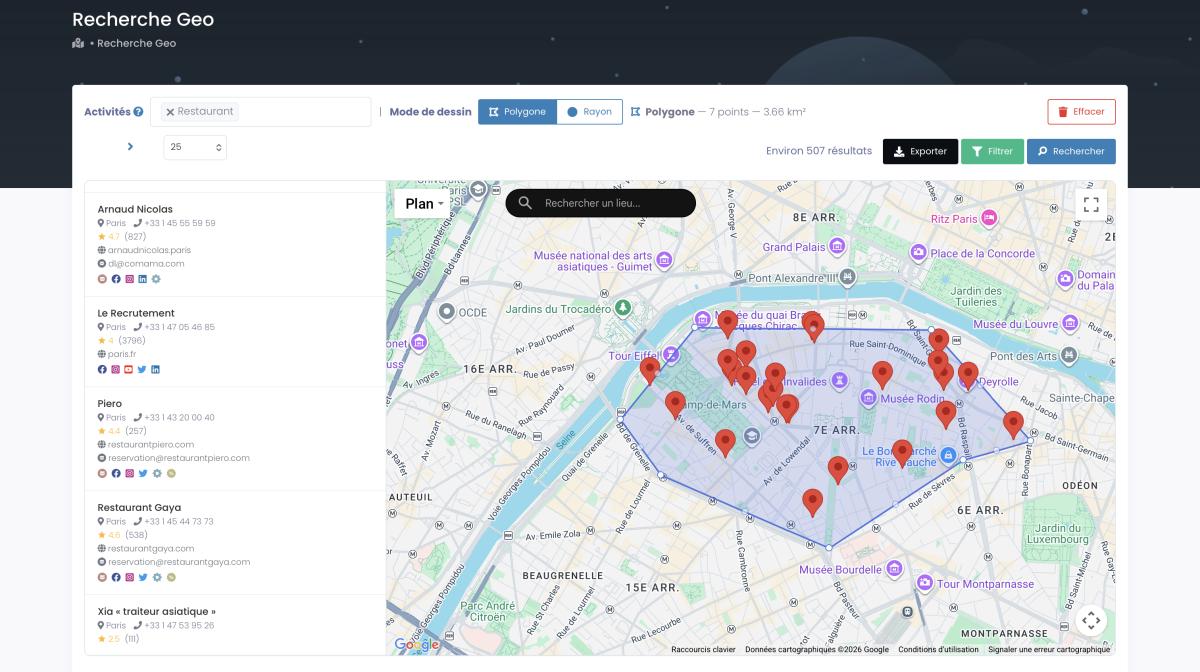

So where are these 161,021 services? Follow the corridors and you've basically got the map.

Border and gateway states dominate — Texas, California, Florida, New York. No mystery there. Those states hold the largest immigrant communities sending money home, and the World Bank corridor data (Mexico, Central America, the Caribbean leading the way) lines up almost perfectly with where the storefronts cluster. Los Angeles, Miami, Houston, New York City: dense, competitive, well-funded.

But the density-per-capita story is sneakier. Some mid-size cities with a specific ethnic concentration have wild ratios of services to residents — and almost nobody is emailing them. Less inbox competition, more warmth. With GeoSearch you're not stuck with state lines either: draw a radius around a neighborhood, or sketch a polygon around a precise corridor that doesn't match any administrative boundary.

Why does any of this matter for outreach? Because a Western Union agent in rural Nebraska and an independent operator in downtown LA share a category and nothing else. Geographic targeting lets your message actually fit the recipient. That's the difference between a campaign and a guess.

B2B Use Cases: Who Targets Money Transfer Services?

So who's actually buying a money transfer service email list? Wider crowd than you'd guess — and it's heavily skewed toward compliance.

Anti-money-laundering and KYC vendors are the obvious whales. Every money services business needs sanction screening, identity verification, and transaction monitoring, and the rulebook gets thicker every year. The named players going after exactly this audience:

- FinScan — AML and sanction screening built for MSBs, advertising 99% straight-through processing and a 62% cut in false positives.

- Alessa — an AML platform with a dedicated "MSB compliance" module and real-time name screening.

- ComplyAdvantage — London-based AML with machine-learning screening and onboarding/transaction-monitoring APIs aimed squarely at fintech and money transfer.

- iDenfy — KYC/AML with guides written specifically for MSB operators.

- NICE Actimize — a heavyweight in AML and fraud, with published analysis on "AML for MSBs and FinTech."

Beyond compliance, the buyers fan out. Payment processors hunting better rates. Fintech and API providers chasing integration partners. Marketing agencies — money transfer shops still run heavily on word-of-mouth, so there's real upside. And the unglamorous-but-steady crowd: CRM, accounting, scheduling, the boring software that keeps a storefront running.

The pattern across all of them? They don't want 100,000 random emails. They want a tight, filtered slice — the right operators, in the right states, with verified contact info. That's financial services email list building done right, and it's the same discipline behind any niche play — the kind we use for financial services email lists targeting advisors, or building niche email lists for accountants. Adjacent categories, same method, one growing cluster.

One more thing, and it's a soft warning: this industry runs on trust. Cold email opens the door. Relationships close the deal. Compliance software for money transfer isn't an impulse buy — lead with that you actually understand BSA, MSB licensing, and corridor-specific headaches, and you'll get further than any clever subject line.

Fresh Data Extraction vs Purchased Email Lists

Time for the head-to-head. The fresh data vs purchased email list debate gets settled fastest with one company's real test.

A payment processor I work with ran both approaches at the same volume — 10,000 contacts each — and tracked them to the qualified-conversation level. The numbers below are illustrative of that single test, not an industry guarantee. But they rhyme with everything I've seen.

| Metric | Purchased List | Fresh Google Maps Data |

|---|---|---|

| Email bounce rate | 23% | 7% |

| Active & correctly categorized | ~69% | ~94% |

| Response rate | 12% | 28% |

| Qualified conversation rate | 2% | 11% |

| Cost per qualified conversation | $133 | $23 |

$23 against $133. That's not a close match — that's a different sport.

And the qualitative gap is even bigger than the table shows: with a purchased list you're often the sixth vendor that month pitching the same recipient off the same recycled database. With fresh data you might be the first human they've heard from in weeks.

The mechanism behind the gap is the filter. Scrap.io applies your filters before credits are spent — so out of 161,021 services you keep only the 106,658 with an email present, and you pay for nothing else. Want only mobile numbers for SMS? Toggle it. Only listings without a website, for an agency play? Done. That's structurally impossible with a frozen file someone sold you. For the full mechanics, here's the complete Google Maps scraping guide.

Don't take the table on faith. Extract 100 fresh money transfer contacts, run a real campaign, and compare the bounce rate to your last purchased list. Test it yourself — your first 100 leads are on us.

Legal Compliance: GDPR, CCPA, and Financial Regulations

Here's the elephant. Legal compliance in financial-services email isn't optional, and the stakes run higher than almost any other sector. Is it legal to email money transfer businesses? Yes — in B2B, with public data, done properly. Let's be precise about "properly."

Federal oversight runs through FinCEN, which means these businesses are touchy about unsolicited contact and you should respect that. State money transmitter licenses add another layer — many states publish their licensees, like California's DFPI directory of money transmitters, which is a useful authority reference (though it carries zero emails and no method). International rules bite the moment EU corridors are involved.

What this means in practice: your data source matters more here than anywhere. A murky purchased list is a complaint waiting to happen. Public Google Maps data, traceable to its origin, is defensible. GDPR compliance follows almost automatically when you're only using information a business published itself; CCPA carves out publicly available business data on the same logic; CAN-SPAM just wants honest headers, real sender ID, and a working opt-out.

For the full legal breakdown — and to settle whether is cold emailing legal for your exact case — read our piece on is cold emailing legal. And a counterintuitive bonus: compliance officers respect vendors who clearly understand their regulatory world. Demonstrate it in your first email and you build credibility instead of friction.

Getting Started: Your Money Transfer Email List Strategy

Want a list that converts? Here's the actual sequence.

Target geographically first. Don't try to email all 161,021 services at once — that's masochism, not strategy. Pick the states where your solution lands hardest. Texas and California alone give you enormous volume.

Split by category. Dedicated operators get one message; convenience-store side-hustlers get another. Same product, different angle, because their problems aren't the same.

Filter before you spend. This is the non-negotiable step. Toggle "email present" and you're working from the 106,658 contacts that can actually be reached — zero credits burned on dead-ends. Extracting a whole country in two clicks, no code, is the entire point; one Scrap.io user pulled 11,734 businesses in 45 minutes. If you're new to the mechanics, here's how to find emails on Google Maps.

Verify, then send. Even fresh data deserves a quick pass — verify your email list for deliverability before launch. Bounce rates wreck sender reputation faster than anything.

Then lead with knowledge. "Hi [Name], noticed your [location] storefront — with [specific regulation] hitting money transmitters this year, here's how operators like you are handling [outcome]. Worth fifteen minutes?" Specific beats slick. Every time.

Run your first extraction the smart way. Filter "email present" before spending a single credit, and pull only the money transfer services you can actually reach. Start free on Scrap.io — 100 leads included.

Frequently Asked Questions

How many money transfer services are there in the US in 2026?

There are 161,021 money transfer service establishments in the United States as of June 2026, according to live Google Maps data from Scrap.io. About 106,658 of them have an email address on file, which you can filter for before extracting.

Is it legal to email money transfer services for business purposes?

Yes. B2B email to money transfer services is legal when you use publicly available contact information and follow GDPR, CCPA, and CAN-SPAM rules. Because the data comes from public Google Maps listings, every contact is traceable to its source. See our cold email compliance guide for the specifics.

What's the difference between fresh data and a traditional email list?

Fresh data is extracted from Google Maps in real time, so contact details reflect what's live today. Traditional purchased lists are static snapshots — often 3 to 12 months old — frequently containing businesses that have closed or changed hands. In one head-to-head test, fresh data cost $23 per qualified conversation versus $133 for a purchased list.

Who targets money transfer services for B2B sales?

Mostly AML and KYC compliance vendors (FinScan, Alessa, ComplyAdvantage, iDenfy, NICE Actimize), plus payment processors, fintech and API providers, marketing agencies, and business-software companies selling CRM, accounting, and operational tools.

How compliant are money transfer service email lists?

When sourced from public Google Maps listings through Scrap.io, they're GDPR- and CCPA-compliant, because they use only publicly available business information that companies chose to publish themselves. Every data point is traceable to its origin.

What's the typical response rate for money transfer service outreach?

Fresh, well-targeted data tends to generate 25–35% open rates and roughly 8–15% response rates — well above purchased lists, which often sit below 10% because of data decay and poor categorization.

How often should a money transfer service email list be updated?

Monthly at the absolute minimum, given how fast the sector churns. Ideally you pull fresh data at the start of each campaign — real-time extraction from Google Maps keeps the list current as businesses update their listings, so there's no separate refresh cycle to manage.

Stop paying broker prices for lists that bounce. 161,021 US money transfer services, 106,658 with email, pulled live from Google Maps and filtered before you spend a credit — GDPR- and CCPA-compliant, traceable to the source. Try Scrap.io free for 7 days, with your first 100 leads included. Start your free trial now.

Generate a list of money transfer service with Scrap.io